Lender Strategy | Philippine SME Financing Guide

The 12 Most Common Mistakes Filipino Founders Make in Lender Meetings — And How to Fix Them Before the Next One

A Preparation Guide for Philippine SME Founders

By Adriel Maniego · Updated June 23, 2026

The short version

In our experience working with founders preparing for Philippine lender meetings, roughly 7 out of 10 rejections trace to preparation, not credit quality. The 12 mistakes below cluster into three categories — preparation failures, expectation failures, and positioning failures — and all 12 are fixable before the next meeting. The structural mistakes can be learned from this article. The conversational calibrations — talk-listen ratios, weakness disclosure timing, live reads on the specific lender across the table — are the work bespoke preparation does directly with founders.

About

Buhay Platforms Inc. is a SEC-registered fintech firm (Reg. No. 2025010186147-22) and a Manila Bulletin Newsmaker of the Year. 100+ financing deals supported nationwide. Network of 30+ financial institutions — commercial banks, rural banks, and non-bank financial institutions. Accredited by the Quezon City, Cebu, Metro Angeles, Pampanga, and Manila Chambers of Commerce and Industry.

We have sat across the table from hundreds of founders preparing for management meetings with Philippine financial institutions — banks and NBFIs alike. Across those preparations, the same mistakes appear so consistently that they have become diagnostic. None are failures of business quality; they are failures of preparation, expectation, and positioning. The good news: all three are fixable, and most of the fix happens before you sit down.

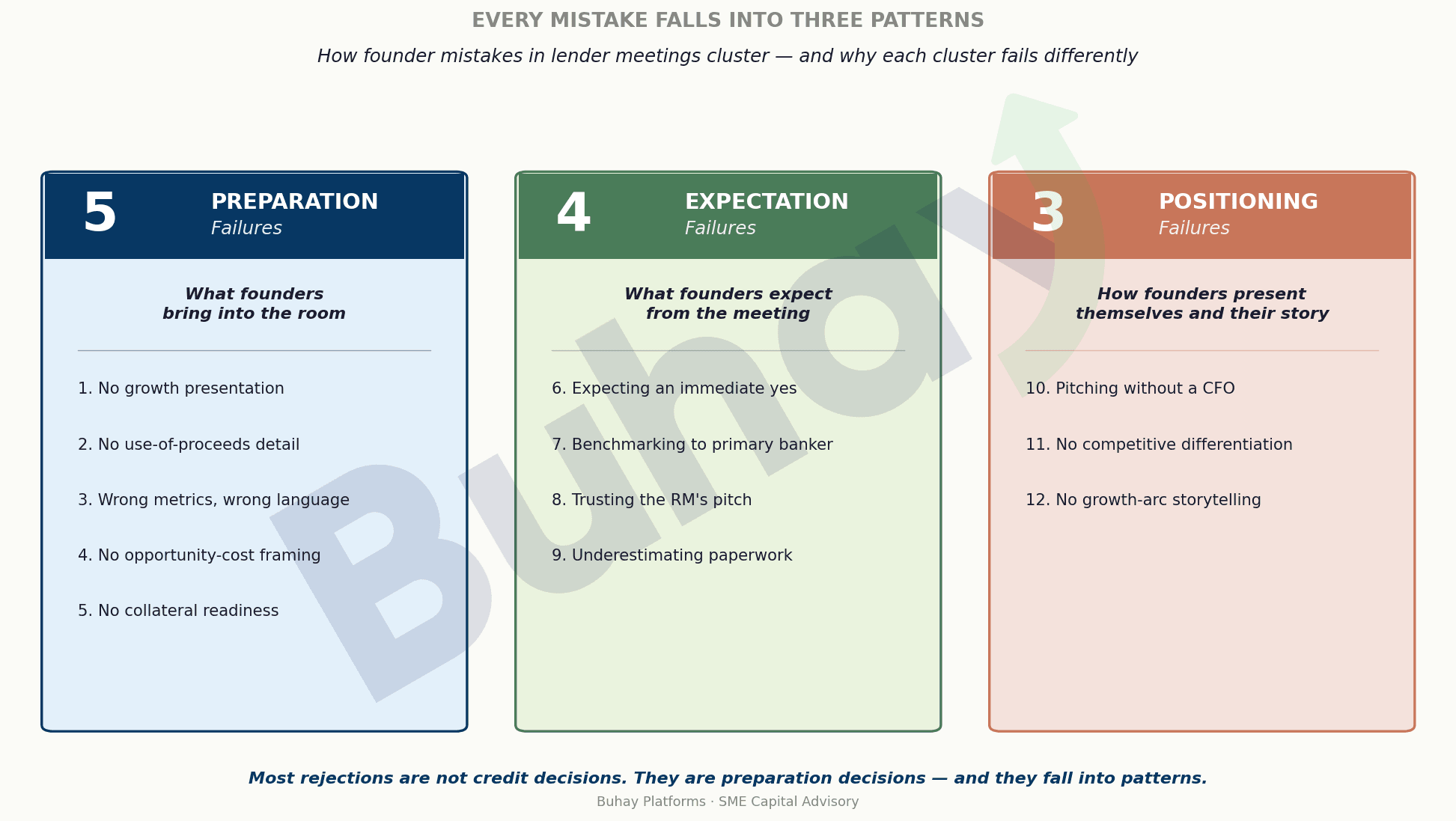

The mistakes fall into three patterns. For each, here is what founders do, what the committee actually takes from it, and what to do instead.

Part One — Preparation Failures

What you bring into the room.

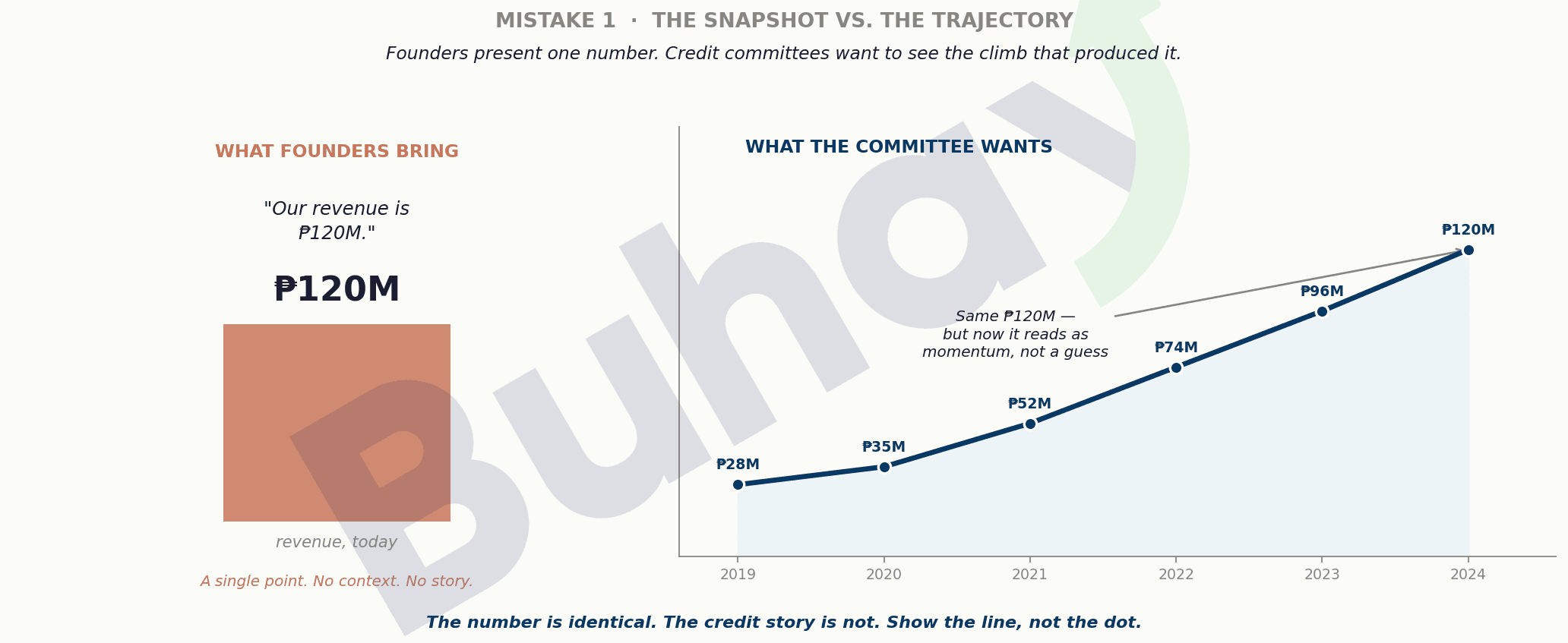

Bringing a snapshot instead of a trajectory

A committee does not lend against a number. It lends against a direction.

- What founders say

- “Our revenue is ₱120M, our margin 22 percent” — a single point in time.

- What the committee hears

- Is this momentum or a plateau? With nothing to tell them, they price the uncertainty as risk.

- What to say instead

- “We climbed from ₱28M to ₱120M over five years.” The slope is the story, not the endpoint.

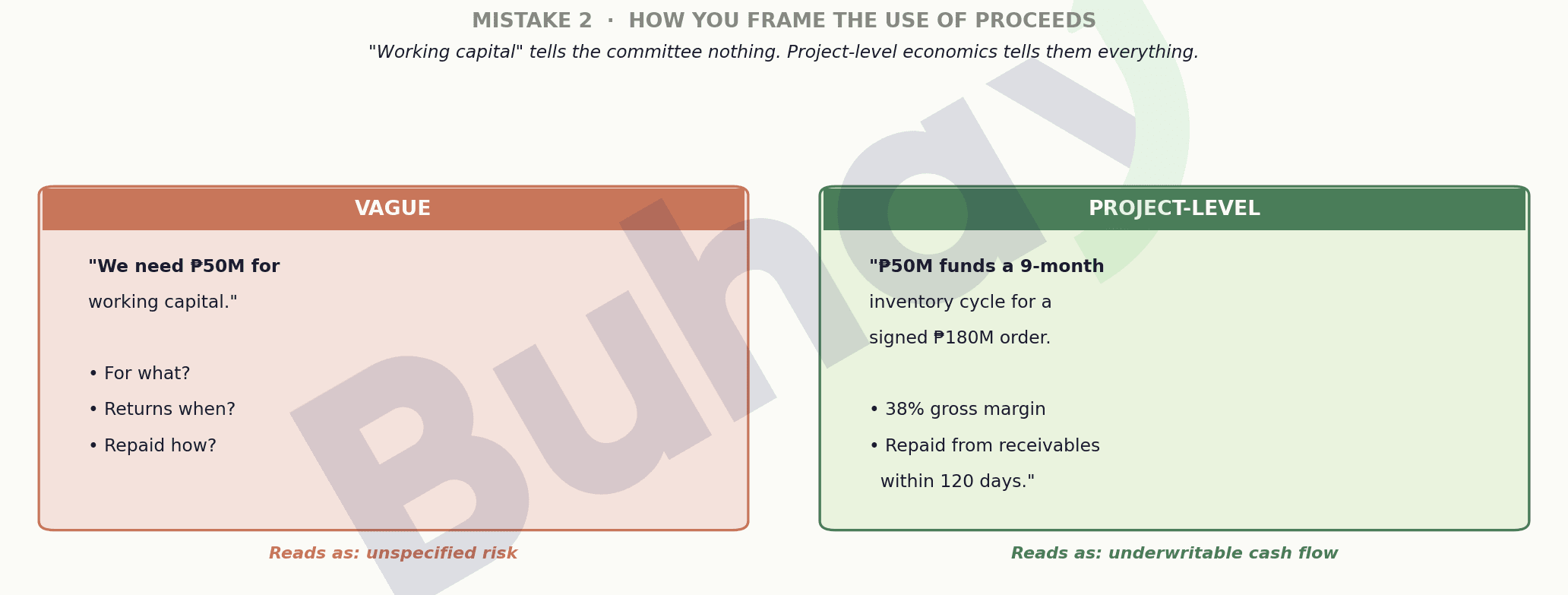

Describing the use of proceeds in vague terms

Unspecified use reads as unspecified risk — the most damaging sentence in a lender meeting is a vague one.

- What founders say

- “We need ₱50M for working capital.”

- What the committee hears

- For what? Returning when? Repaid how? Nothing here can be underwritten.

- What to say instead

- “₱50M funds a nine-month inventory cycle against a signed ₱180M order at 38% margin, repaid from receivables within 120 days.”

Speaking the wrong financial language

When a founder cannot translate performance into the committee’s vocabulary, the committee translates it for them — conservatively.

- The mistake

- Describing the business in customer-and-supplier terms: units sold, market share, product quality.

- The fix

- Speak the committee’s language: debt-service coverage, working-capital cycle, customer concentration, leverage. Translate before they do.

Failing to frame the opportunity cost

Committees fund opportunities far more readily than needs — a need signals weakness; an opportunity signals upside the bank can share in.

- What founders say

- “We need the financing to keep operations running through the lean months.”

- What the committee hears

- This business is undercapitalized and may struggle to service new debt.

- What to say instead

- “We turn away ~₱40M in orders a year for lack of inventory funding. This facility converts that backlog into revenue at our current margin.”

Arriving without collateral readiness

Discovering security problems mid-process stalls the deal and signals disorganization.

- The mistake

- Mid-process, titles aren’t clean, receivables aren’t documented to register, equipment has no recent valuation.

- The fix

- Before the first meeting, know exactly what you can pledge and what condition the documentation is in. Readiness itself is a signal.

Part Two — Expectation Failures

What you expect from the meeting.

Expecting an immediate answer

A new credit relationship moves at committee speed — weeks, sometimes months.

- The mistake

- Expecting primary-banker speed, then reading the delay as disinterest and disengaging.

- The fix

- Calibrate to the institution’s clock. Persistence through that window is exactly what pays off.

Benchmarking everything to the primary banker

The primary banker has years of history and personal trust; a new institution has none of that.

- The mistake

- Expecting a new bank to match the terms, speed, and trust of a decade-old relationship.

- The fix

- Treat the new relationship as starting at zero — it earns its way up. (That is what Mistake 12 is about.)

Trusting the RM’s pitch as a commitment

A relationship manager’s job is to present the institution favorably and bring deals in — not to underwrite them.

- The mistake

- Anchoring on the ₱100M an RM floats early — then feeling deceived when the term sheet says ₱15M.

- What’s really happening

- That was marketing, not a commitment. A realistic first facility at your scale is ₱10M–₱30M.

- The fix

- Ask directly: “What’s the average first facility you’ve booked with a company at our revenue scale in the past 12 months?”

Underestimating the paperwork

A new institution compensates for the absence of relationship history with documentation.

- The mistake

- Expecting phone-call ease, then giving up partway through the document load.

- The fix

- Treat the package — 3 years of audited statements, bank statements, clearances, project economics, deployment plan — as the committee’s substitute for history. A clean package signals readiness no pitch deck can.

Part Three — Positioning Failures

How you present yourself and your story.

Pitching without a CFO, in the only voice you know

A client conversation is about value; a supplier conversation about cost; a lender conversation about risk and trust.

- The mistake

- Pitching in client-and-supplier sales language — which sounds like selling, and committees distrust selling.

- The fix

- Speak risk and trust: cash-flow predictability, customer concentration, debt-service capacity. Name what could go wrong before they ask. Sound like a CFO even without one.

Failing to articulate differentiation in credit language

Each kind of competitive advantage is read differently by a credit committee.

- What founders say

- “We win because we offer 90-day terms to our buyers.”

- What the committee hears

- A structurally longer working-capital cycle. More capital to fund the same revenue. A risk signal.

- What to say instead

- “Our reject rate is under 2% vs an 8% industry average — which is why our two largest customers grew orders 60% year on year and retention sits above 95%.”

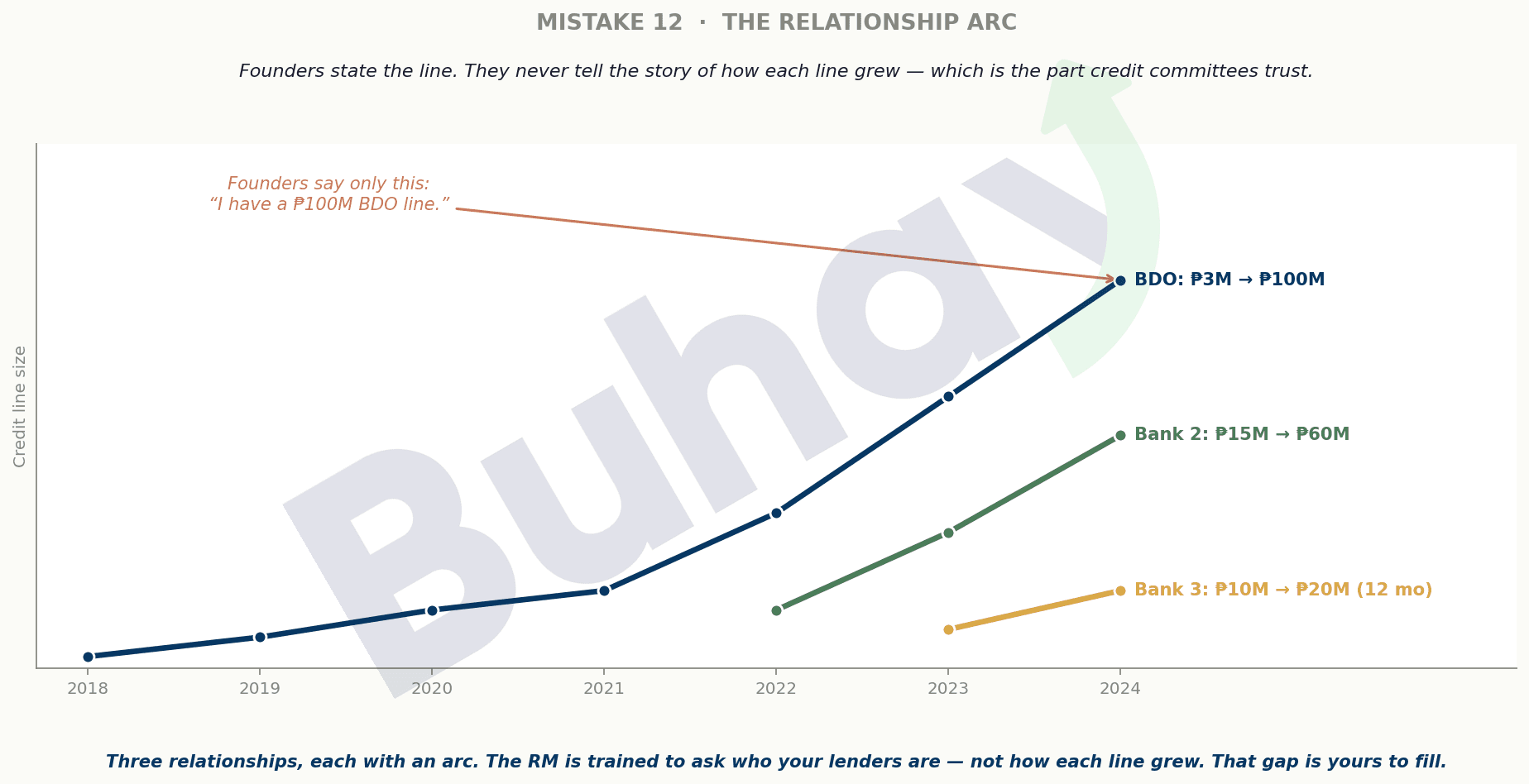

Stating the line instead of telling the arc

The story of how a facility grew is the part a credit committee trusts most — and the part founders leave out.

- What founders say

- “I have a ₱100M line with BDO.”

- What the committee hears

- A static figure with no history. The RM notes it and moves on.

- What to say instead

- “We grew BDO from ₱3M in 2018 to ₱100M by 2024; added a second bank at ₱15M in 2022, now ₱60M; a third a year ago at ₱10M, already ₱20M.” Other lenders’ rising conviction is your strongest proof.

The meeting is won in the preparation

None of these twelve are about whether your business is good enough. They are about whether the conversation you walk into is the one the committee is actually having. The founders who break through to seven, eight, ten institutional relationships are not running dramatically better businesses — they are running better-prepared conversations. The business sets the ceiling; the preparation determines how much of it you reach.

If you want to pressure-test your story before you walk in, this is the work our advisory team does with founders — mapping your financials, differentiation, and relationship arc into the committee’s language. It pairs with our companion guide, NBFI vs. Bank: how to pitch each lender type.

“The meeting is rarely won in the room. It is won in the preparation.”

Frequently Asked Questions About Philippine Lender Meetings

Preparation, not credit quality. Roughly 7 out of 10 rejected applications fail because the founder treated the meeting as a test of their business rather than as a test of their preparation, sophistication, and institutional readiness. The committee evaluates the founder as a long-term credit relationship, not just the financials on the page.

Eight to twelve weeks from first meeting to approval is typical for a Philippine commercial bank. The first three to four weeks are usually silent — that silence is part of the process, not a signal of rejection. NBFIs decide faster, often within five to ten business days, because the decision-maker is in the room rather than escalating through multiple committee layers.

For most Philippine SMEs in the ₱50M to ₱500M revenue range, the realistic first facility from a new institutional bank is ₱10M to ₱30M, regardless of what the existing primary banker offers. New relationships start at a different point than mature ones — pushing for parity with an established line damages credibility before the relationship has a chance to start.

A new institutional facility typically requires three years of Audited Financial Statements, six months of bank statements across all primary accounts, BIR Form 2316 and corporate registration documents, CMAP and NFIS clearance certificates, a one-page executive summary written for the credit committee, project-level economics for the proposed deployment, customer and supplier reference lists, and a deployment plan with sensitivity analysis. The documentation volume is the credit committee’s way of compensating for the absence of historical relationship.

Tell the arc, not the line. Stating that you have ₱100M with your primary bank gives a new credit committee a static profile they could have gotten from a directory. Walking through how the relationship started at ₱3M and grew over years gives them a demonstrated track record of scaling credit responsibly — which is the single most valuable signal a new institution can receive.

Key Takeaways

- Most rejections are preparation decisions, not credit decisions — roughly 7 out of 10.

- Tell the arc of your existing lender relationships, not just the current line size.

- The structural mistakes are learnable from this article. The conversational calibrations require bespoke preparation.

Pressure-Test Your Story Before You Walk In

Buhay works with founders preparing for management meetings — mapping your financials, differentiation, and relationship arc into the committee’s language, across a network of 30+ banks and non-bank financial institutions. Start with a complimentary assessment.

Adriel Maniego

Founder & CEO, Buhay Platforms Inc.

Buhay — Manila Bulletin Newsmaker of the Year

Accredited, QC, Cebu, Metro Angeles, Pampanga & Manila Chambers

[email protected] · [email protected] · buhay.com.ph

SEC Reg. No. 2025010186147-22.

This article is for general informational purposes and does not constitute financial, legal, or investment advice. Figures are illustrative. Founders should consult qualified professionals before making lending decisions. © 2026 Buhay Platforms Inc.